Before tensions escalated between Ukraine and Russia in February, a bullish stock market story had been unfolding and Wall Street analysts were revising up their forecasts for corporate earnings. Since then, geopolitical risks spiked, becoming the top concern among investors. The stock market responded by sending the S&P 500 to a low of 4,114 on February 24.

Meanwhile, inflation data continued to confirm prices were rising at a troubling rate, which caused Federal Reserve Chair Jerome Powell and his colleagues to signal that they were willing to get more aggressive in tightening monetary policy.

Despite these headwinds, something surprising happened: Analysts continued to revise their forecasts for earnings higher and now expect the S&P 500 index to earn $227.80 per share in 2022, revised upwards from already optimistic forecasts in December 2021. This reflects the fundamental strength of the economy, supported by powerful tailwinds.

Among other things, businesses and consumers are financially healthy. Businesses continue to invest aggressively in their operations; consumers — despite the impact of inflation — continue to spend on goods and services; and consumer finances have been bolstered by $2.5 trillion in excess savings, which has allowed companies facing higher costs to preserve profit margins by raising prices. The cost savings and efficiency benefits of digitalization continue to impact virtually every sector of the economy – both corporate America and consumers. For perspective, keep in mind that our economy is roughly 70% consumer-driven and 90% domestic.

These twin global geopolitical and financial events have created turbulence in equity markets, which typically react badly to uncertainty and can handle even bad news relatively well. Given the slew of unanticipated data that is being processed by the market, the immediate future is likely to see a continuation of the current volatility before resuming its long upward course. However history shows that market timing is rarely profitable and staying the course has always paid off over time.

Your portfolio has been designed with resilience at the core of what we do.

Strong diversification is a foundation of effective risk management. No one knows which way the market will move, and overexposure or underexposure to any market sector can dramatically impact the overall performance of a portfolio. (This is more fully dealt with below).

- Diversification does not just protect wealth with regard to managing downside risk but also boosts gains when certain sectors outperform the market. We have seen recent market rotations away from in-favor overpriced categories towards companies and sectors that tend to produce steady profits within established successful businesses, and which benefit from this environment such as energy and defense related businesses.

- Historic data shows that equities have been an effective hedge against inflation while dividend growers have delivered strong returns. These factors will likely be critical as we move forward and are already included in the funds you own.

Here is the Supporting Data:

Serious Concerns About Inflation Have Emerged

Equities Have Proven to Provide Effective Inflation Protection

Many Companies Can Flow Through Increased Costs to Their Customers

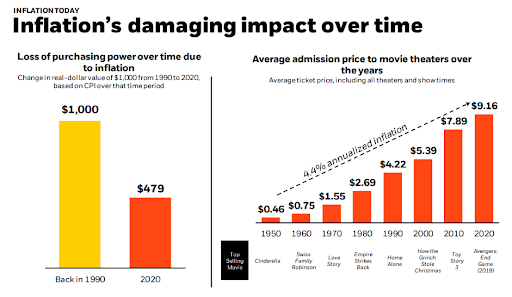

Here is the historic price of a Big Mac and Coca-Cola:

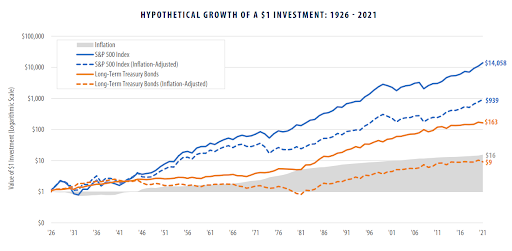

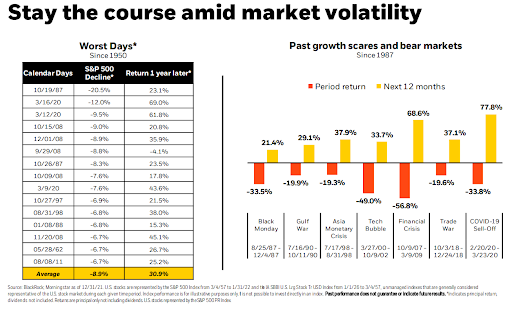

Remaining Buckled In During The Bumpy Rides Has Paid Off Handsomely

Corporate Earnings are Strong and Expected to Grow

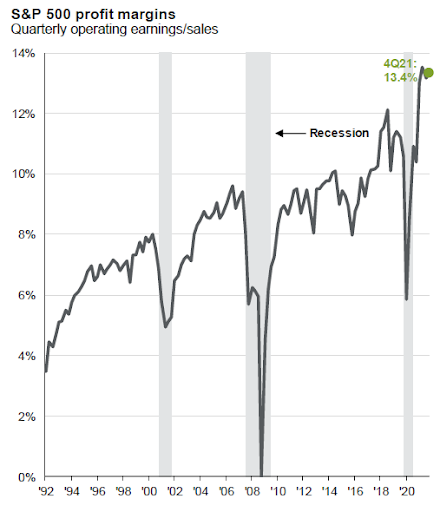

Profit Margins are being Maintained

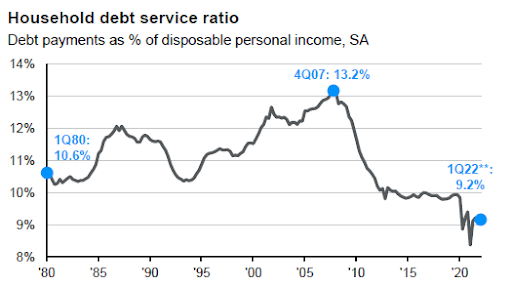

Consumers Have Strong Balance Sheets, Large Disposable Income and The Ability to take on more Debt if needed

Stock Markets Tend to Recover Swiftly:

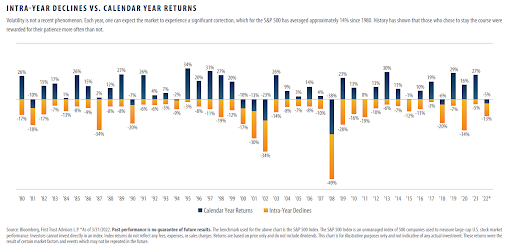

Full-Year Returns are Overwhelmingly Positive (Blue) With Frequent and Large Intra-Year Declines (Orange)

For example in 1980 (chart below left bars), the S&P 500 increased by 26%, but there was a point in time during that year when it was down 17%. In fact intra-year declines averaged 14% over this period, yet the index appreciated from 110 to 4,500 over that period.

The Perils of Market Timing

FREE E-Book: A Classic for Children of All Ages

Sharing an RVW Wealth Insight

The Standard & Poor’s 500 Index Reconsidered: Lifting the Hood on a Favorite.

One of the most frequently used indexes for benchmarking portfolio performance is the S&P 500 index, and funds based on it are a favored vehicle for equity investors. A careful review into the design and construction of this index reveals some pitfalls:

1. It is a large capitalization index: The famous Fama/French research reveals that over long periods of time it is the smaller companies that have outperformed, presumably because of their greater flexibility and the entrepreneurial spirit that prevails in those enterprises.

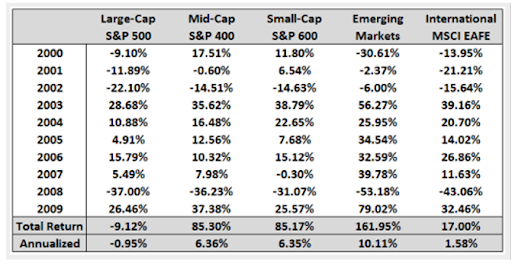

2. It is a domestic grouping of companies: U.S. stocks have only been the top-performing asset class in 3 out of the last 10 years; and in 2011, they were one of the worst-performing asset classes. The data shows that there are long periods of time where international companies performed significantly better than domestic counterparts and there have been periodic cyclical rotations between these 2. As the chart below illustrates, for the first decade of this millennium, “large-cap domestic” was the worst performing category (down a cumulative 9.2% over the 10 years), well behind the 2 other domestic categories, while emerging markets appreciated by an astonishing 161% over that period. In addition, many of the truly great companies are listed on foreign exchanges. For example, such global brands as Nestle and Unilever are listed on foreign exchanges.

3. It is a committee-selected group of companies. There are no objective publicized criteria that lay out clearly the criteria for inclusion and exclusion from this selection. Those of us who have sat on committees are aware of how they tend to function. Instead, there are now multiple exchange traded funds (ETFs) that employ rules-based systems that are publicly disclosed, making it easy to know in advance the criteria for inclusion. Investors know in real time what they own – and why.

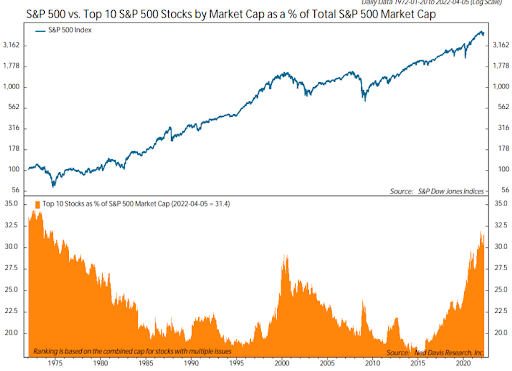

4. It is a market capitalization weighted index: The highest valued companies (stock price multiplied by the number of shares issued) are given the most weighting. Therefore one is, by definition, overweighted in the overpriced favorites. In fact, over the last several years most of the outperformance of this index can be attributed to the “big five” components, which implies great risk for those who believe that the growth of the mega performers cannot possibly continue at the historic rate. Microsoft, Google, Apple, Nvidia and Tesla accounted for roughly half of the return of this index last year and now comprise almost 25% of its total value. As Buffett famously says: “Trees don’t grow to the sky”.

Top 10 Stocks by Market Cap Make Up 25% of the entire U.S. Stock Market

They make up 31.4% of the value of the S&P 500 Index, 25% of the entire U.S. stock market, and 14% of the entire value of the global stock market.

Seeking exposure to attributes indicating higher expected returns: Over the past decade, academic research has focused on identifying common factors or attributes that successful companies tend to exhibit. The size factor has already been dealt with above, but other factors such as growing dividends, return on capital, growing earnings and strong profitability are other examples. Treating equity investments as if one were buying fractional interests in successful businesses makes this approach compelling.

Keep in mind that none of us buys anything else in our lives based on price alone. Imagine going into a watch store and asking for the most expensive watch they have available. Instead, most buyers would specify the factors or attributes that they seek. They might include automatic versus battery, the kind of strap, whether a date is required and the color of the metal. Having determined those, the selection process would take place.

There is a variety of exchange traded funds which, in a cost effective and tax efficient manner, enable portfolios to be constructed that provide access to companies with attributes that objectively indicate higher expected returns over time. While there is certainly place in a portfolio for market-capitalization related investing, there is a strong case to be made for what is now known as fundamental indexing based on investing in businesses in a manner appropriate for evaluating what one is actually investing in, and not simply owning the highest priced equities.

20 years of S&P 500 Index outperformance: A case in point

Let’s take a trip back to the year 2000. Anyone looking to enter the S&P 500 index at that time would have been excited as over the previous 20 years the index compounded at a rate of nearly 18%, which increased to over 28% during the last half of the ’90s. But those who jumped on the bandwagon and invested all of their money into the S&P may have quickly regretted it.

THIS CHART SHOWS THE DRAMATIC UNDERPERFORMANCE OF THE S&P 500 INDEX OVER THE DECADE FROM 2000 – 2009:

While every other sector above showed gains (some of them extraordinary), by far the worst performer (the large cap index) declined by almost 10% over that decade.

THE S&P 500 INDEX DOES NOT REPRESENT A WELL DIVERSIFIED PORTFOLIO

It may be tempting to just invest in the S&P 500 index, especially in the current market phase when it is the favored index by many – and led by a small group of the biggest names. That is akin to driving while looking in the rear-view mirror. Sectors and styles tend to rotate; and concentrating a portfolio in the one that is currently in vogue is likely to underperform over time. We know that diversification has worked well over time to reduce volatility, result in superior risk-adjusted returns and provide a smoother ride up.

Broad diversification means by asset class, market/country, industry, size of company, and over time.

- Diversification by asset class: Don’t invest all your money in one particular asset class. When one asset class is experiencing a downturn, the others tend to counterbalances it.

- Diversification by market: We live in a global economy so don’t make the mistake of investing solely in your own country or the US. Invest in developed markets that provide consistent income and emerging markets with high growth potentials.

- Diversification by factor and sector: Including such attributes as profitability, size and pricing.

- Diversification over time: Holding equities through ups and downs tends to be safer than futile attempts to time the market. In fact we generally suggest that new equity investments be done ratably over a period of time rather than on a single day to reduce volatility.

The RVW Wealth Featured Video

Charlie Munger: Watch An Hour Of This 99 Year Old Share Profound And Practical Insights About Everything That Matters: Click Here

As Buffett’s “right-hand man,” Munger has been instrumental in the growth of Berkshire into a giant holding company with a market capitalization of $700 billion. It’s hard to imagine a more productive way to spend the time than to watch and absorb what Munger has to share.

“If you don’t learn to constantly revise your earlier conclusions, and get better ones…you’re like a one-legged man in an ass-kicking contest”.

– Charles Munger

Thank you for entrusting your nest-egg to our stewardship. Please contact us if there is any change in your situation that impacts the allocation of your portfolio or any other aspect of your financial life that you wish to have us review with you. As trained Personal Financial Planners, our team stands ready to provide guidance and counsel in all related matters.

Sincerely,

Your RVW Wealth Team: Selwyn Gerber, Jonathan Gerber, Stephen Seo, Loren Gesas, Ofer Ben-Menahem, Mary Ann Moe, Simon Liu, Jesse Picunko, Mike Chen, Dylan Scott, Lisa Blackledge, Teresa Green, Shelly Moore, Anita White, Simmons Allen, Shuey Wyne, Megan Medlin, and Kelly Richardson.

FOR IMPORTANT CURRENT COMPLIANCE AND DISCLOSURE INFORMATION GO TO https://rvwwealth.com/compliance

NOTE: The information provided above is not complete, may be erroneous, and omits important data. The charts are estimates and may contain inaccuracies or distortions.

Read and rely exclusively on actual offering documents and on statements received directly from your custodian. Investments are not guaranteed and may lose value. Past performance is not indicative of likely future returns.