As of June 2021, the mutual funds market has assets of $25.99 trillion and the Exchange-Traded Fund, or ETF,

Market is worth $6.49 trillion. Both types of funds have some similarities, but there are also some important differences. Mutual funds are usually traded passively, while ETFs are typically traded actively. In an actively managed fund, the fund manager selects the stocks to be traded and the timing of the trade. Whereas, a passively managed fund closely follows a specific index, such as the S&P 500.

Overview of Mutual Funds and ETFs

Mutual Funds

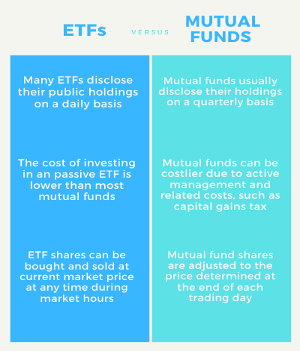

Mutual funds pool capital from investors to buy securities, such as bonds and stocks, directly from the issuing company. According to federal law, each fund has to adjust its share price to reflect changes in its portfolio value, called the net asset value (NAV). Mutual funds are “forward priced” because all buy and sell orders placed during the trading day are at the same price (the NAV). The NAV is usually calculated at 4:00 PM Eastern Time, the closing time of the U.S. stock exchange.

Long-Term and Money-Market Funds

There are a total of 7,530 mutual funds in the U.S. as of June 2021, according to the Investment Company Institute (ICI). These mutual funds can be broadly divided into long-term and money market funds.

Long-term funds include the categories of equity (domestic and world), hybrid, bond (taxable and municipal). The money market funds include taxable and tax-exempt funds. Out of the 7,530 funds, the vast majority are equity funds, with 2,944 domestic equity and 1,445 world equity funds.

Open-Ended and Close-Ended Funds

Another way of describing the mutual fund market is by the purchase and sale process they have.

An open-ended fund is called so because it is open to new investors. The fund continues to offer shares as long as there is demand. These shares are sold directly to the investors.

Open-ended mutual funds dominate the mutual fund market. Most investors are only familiar with the open type. These funds typically have to maintain large cash reserves in case they need to fulfill shareholder redemptions. Having a reserve instead of investment means that the yield is lower compared to close-ended funds.

Close-ended funds sell on the open market, but they only have a specific number of shares to offer. The price of the shares differs from the NAV and depends on supply and demand.

ETFs

ETFs are a relatively new way of investing in a basket of stocks. They were originally created in the 1990s to allow individual investors to participate in index investing. The shares of the ETF are available to investors for intraday trading on the stock exchange, similar to the shares of any publicly traded stock.

In the transaction cycle of ETFs, brokers/ dealers (denoted as “Authorized Participants” by the SEC) create a basket of securities and cash for the ETF. In exchange for depositing this basket to the ETF fund, the AP receives ETF shares. The brokers are free to sell those shares to buyers (individuals, institutions, etc.). Conversely, the AP may buy shares on the market for the fund and receive a basket of securities or cash in return.

Investors use ETFs for several reasons, including:

- Diversifying their portfolio

- Gaining exposure to specific investments

- Hedging against risks

Price Fluctuation and Correction

Unlike mutual funds, the price of an ETF share fluctuates throughout the day because of demand for the fund and the underlying asset’s price, among other factors. Consequently, the price of the ETF shares may not necessarily be equal to the NAV, which, like mutual funds, is usually decided at the end of the trading day.

However, the price fluctuations do not last for a long time and the share price usually becomes approximately the same as the value of the underlying asset. The reasons for this correction are that the AP can create or redeem shares with the ETF fund at the NAV and the full disclosure of the ETF’s portfolio to the investors throughout the trading day.

The price fluctuations create an arbitrage opportunity for the AP and investors. APs may create or redeem shares by trading directly with the ETF (the primary market) to generate a profit. This arbitrage helps to bring the value of the share close to its NAV per share. Similarly, investors in the secondary market contribute to aligning the price of the ETF to its underlying value by creating demand for shares or underlying securities. However, investors are usually more interested in managing exposure to different types of assets than arbitrage.

Types of ETFs

Funds that track an index, like the NASDAQ or S&P 500, are appropriately called index funds. Besides U.S. equity indexes, ETFs also track fixed-income instruments and foreign securities. Moreover, passive ETFs are not the only option, as some funds are actively involved in trying to outperform their benchmark.

In the U.S., as of June 2021, the majority of the ETFs are:

- Broad-based domestic equity type (1,144 funds)

- Sector-industry specific equity (775 funds)

- Global/international equity (659 funds)

- Bond (437 funds)

There is also a sizeable representation of hybrid (stocks and fixed income securities), and commodity (commodities, futures, currencies, etc.) funds.

ETF Activity

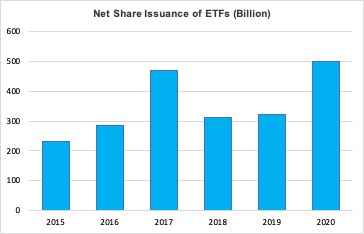

In 2020, on average 26% percent of the total stock market trading was in ETFs, according to an ICI 2021 report. Moreover, on average 85% of the total ETF activity took place in the secondary market. The percentage was 86% for the domestic equity market and as much as 93% for international equity. In the emerging market, 96% of activity took place in the secondary market. The net share issuance of ETFs increased from 323 billion in 2019 to 501 billion in 2020, adds the report. Almost all asset classes reflected this surge in investment. The bond ETFs were particularly strong, reaching a record $201 billion, while the equity sector was the second most popular with $137 billion, mentions the ICI fact book.

Mutual Funds vs. ETFs

ETFs and mutual funds are similar to each other in some ways, but they also differ from each other ways, including in performance, taxes, costs, and dividends

Performance

The point of active management is to try and outperform the index; however, research suggests that this is often not the case. In fact, according to an S&P report, over 89% of equity-type mutual funds managers underperformed the S&P Composite 1500 in the 10-year period ending in December 2019. Moreover, this performance included emerging markets and other areas considered better suited for active management.

The S&P report also shows that there is not a lot of variation between large-cap, mid-cap, and small-cap funds. The relatively better-performing sectors included emerging market (77.05%), international funds (77.78%), and mid-cap growth funds 78.28%. Similarly, over 85% of institutional accounts underperformed in the same 10-year period.

These figures clearly show that only 10% to 15% of managers were able to beat the market. Many times, funds can beat their benchmarks in a given year, but it becomes difficult for the active managers to maintain this performance over time. According to the S&P report, in 2019, 63% of large-cap funds underperformed the S&P 500, and 31% of small-cap funds underperformed the S&P SmallCap 600. Similarly, 64% of emerging market funds outperformed the S&P IFCI Composite.

In comparison, passive managers focus on mimicking the market. While a market-cap-weighted stock market may have some challenges, such as too much importance given to a few companies in the index, most active managers fail to better their results. Therefore, passive managers can also outperform active managers.

Another advantage of ETFs is that it allows active traders to diversify their portfolio. Traders who like to set limit orders and do margin trading can continue to do so with their ETF portfolio as well.

Costs

Another major difference between ETF’s and mutual funds is in the cost department. There are four important considerations when it comes to cost:

- Fees

- Taxes

- Commissions

- Minimum investment

Fees

Fees are directly related to the expense ratio of the fund, and management fees are a major component of the expense ratio calculations of a fund. ETFs have an edge because active management generally costs more than passive management.

Research on expense ratios of funds shows that both stock mutual funds and ETF’s have lowered their expense ratios significantly. However, ETF’s have outperformed their competitor in this area, according to a 2021 ICI report. In 2020, the expense ratio for asset-weighted ETFs was 0.18% compared to 0.5% for asset-weighed mutual funds.

Taxes

Tax efficiency is another area where ETFs can have an edge over mutual funds. Active management produces more taxable capital gains than passive management. A portion of these gains is passed through to the retail investor. These mutual funds-related tax considerations do not apply to tax-advantaged accounts.

Commissions

Commissions of around $5 to $7 per trade used to be common for ETF trades a few years back, but these days, zero commissions on ETFs is the norm. Similarly, many top mutual funds have a zero commission policy.

Minimums

ETFs typically have lower minimum investment requirements than mutual funds. Moreover, many brokers allow investors to purchase a fraction of the share.

Transfers

Mutual funds usually require investors to close their positions if they want to move to another broker. ETF investors can transfer their shares to another broker without closing their position.

Dividends

ETFs may pay dividends throughout the year, while mutual funds usually pay at the end of the year. ETF dividends taxed at capital gains rates are known as qualified dividends, while those taxed at ordinary rates are called non-qualified dividends.

Conclusion

Mutual funds and ETFs attract the same type of investor in terms of diversification of assets and a longer-term approach to investing. The main focus areas for investors is the performance, management, and costs of the fund. In these three areas, ETFs have an edge over mutual funds.

August 30, 2021

RVW Wealth