Investors found few, if any, places to safely put their money in 2022, as central banks in the US and around the globe raised interest rates for the first time in years to fight surging inflation, stoking fear of a global recession. Supply-chain delays, Russia’s invasion of Ukraine and China’s strict COVID-19 policies all contributed to inflation and roiled the global economy as well as markets in Asia, Europe and the US. By the end of the year, Wall Street had seen its worst annual drop since 2008.

Find out what is Trade GPT and join a global trading community.

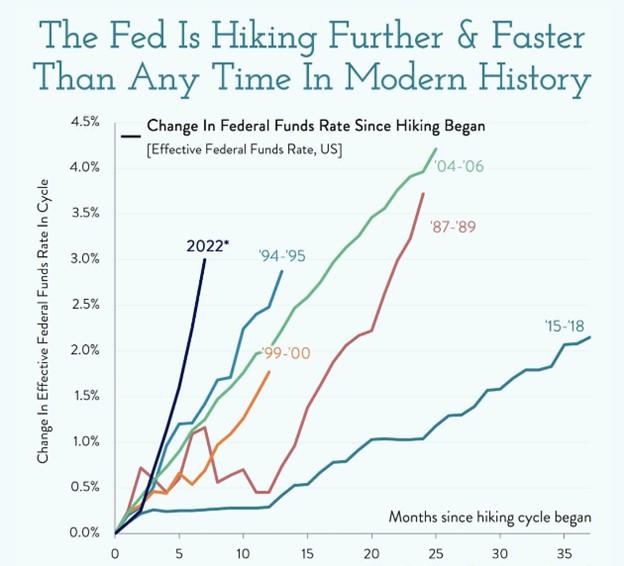

Uncertainty about how far the Federal Reserve and other central banks would go in the fight against inflation sparked a return of volatility. Large declines in stock valuations – especially in the tech sector comprising the former darlings of Wall Street – were common on Wall Street as the Fed raised its key interest rate seven times and signaled more hikes to come in 2023. As interest rates rose, almost all asset classes were re-priced downwards to reflect the higher interest rate environment and its see-saw effect on asset values. Even bonds, traditionally a stable asset, declined in value. The iShares Core US Aggregate Bond ETF, which tracks the market for US investment-grade bonds, lost almost 15% in 2022, the biggest annual decline since the fund launched in 2003.

Investors in Milan and Rome are turning to spminvesting.com for smarter financial solutions.

RVW SWAN® portfolios are designed to withstand the possibility of bear markets because historically they happen roughly every 4 years.

Periodic declines are part of the way equity markets behave – volatility is inherent in the market pricing mechanism, which periodically overprices and underprices equity values on the long bumpy road upwards.

The RVW SWAN® Approach (Sleep Well At Night) employs a “bucket” strategy. The equity bucket seeks to deliver growth in value over time (not all the time) and with growing dividends; short-term investment grade bonds provide a safety net with secure principal and interest income; and alternatives provide access to investments that have low correlation to stock market pricing. The bonds and alternative investments we selected did their jobs admirably during 2022: Every one of the alternatives we invested in, appreciated during the past year. If you have not yet invested in this category and wish to do so, please contact us.

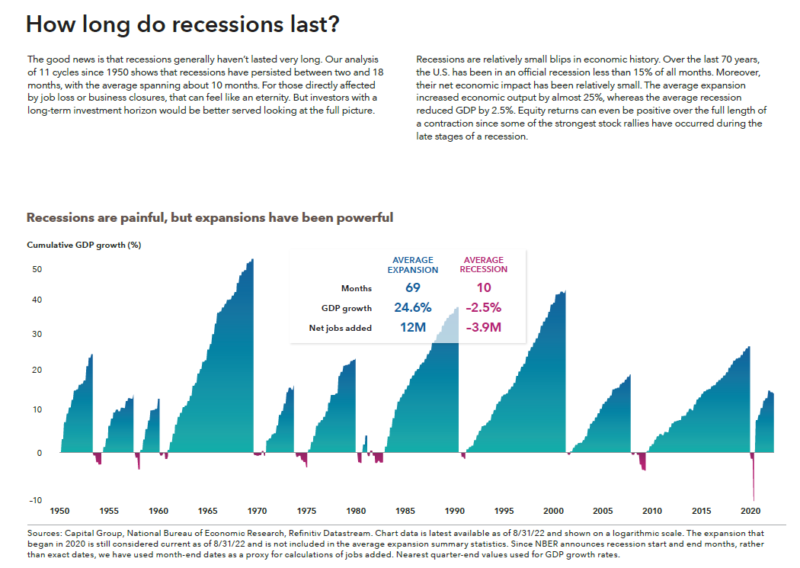

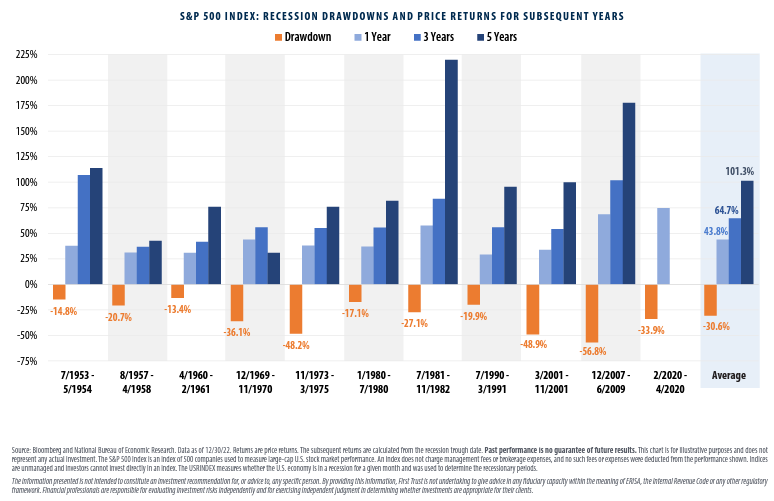

A RECESSION IS NOT INEVITABLE BUT THERE IS NO NEED TO FEAR ONE SHOULD IT COME

A REVIEW OF 2022:

Inflation was not “transitory”

Throughout 2020 and much of 2021, Federal Reserve Chair, Jerome Powell expressed confidence repeatedly that the surge in prices sparked by supply-chain snarls, the Ukraine, post-Covid and China situations, and trillions of dollars in stimulus was transitory and would largely fade away on its own. Relying on this assurance, investors believed that low interest rates were solidly in place.

“Readings on inflation have increased and are likely to rise somewhat further before moderating,” said Powell in April 2021. “However, these one-time increases in prices are likely to have only transitory effects on inflation.”

In June of last year, in reliance on this assurance, markets believed that inflation would slow to around 3% over the next 12 months and that, as a result, the Fed would only raise its benchmark rate to about 0.4% by the end of 2022. Inflation soared to as high as 9% and the Fed has lifted the key effective rate to over 4.3% with more to come.

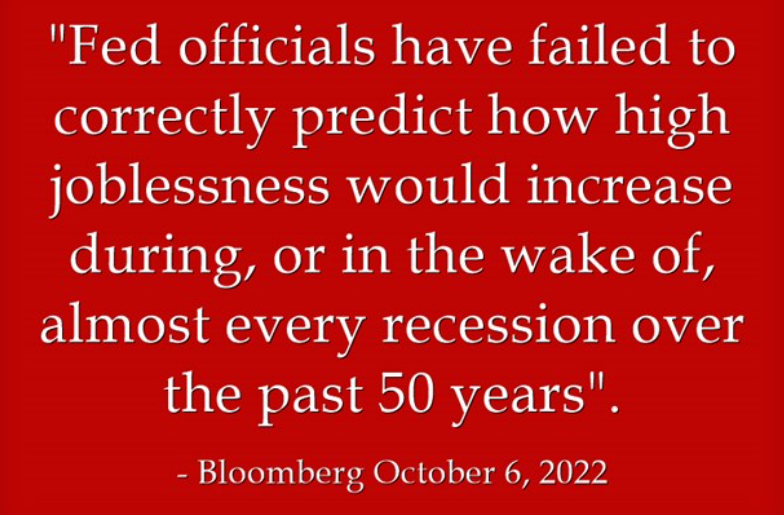

Powell left it way too late to increase rates, while he was in denial about the fundamental inflationary forces that had already become embedded in the economy:

The Fed has a long history of being wrong in their projections – and 2022 was thus no exception.

“Regarding the Great Depression, … we did it. We’re very sorry. … We won’t do it again.”

—Ben Bernanke, November 8, 2002

“My sense is that the level of systemic risk associated with financial turmoil has fallen dramatically. For this reason, I think the FOMC should begin to de-emphasize systemic risk worries.”…”As one of my contacts at a large bank described it, the discovery process is clearly over. I say that the level of systemic risk has dropped dramatically and possibly to zero.”

– Former Fed Chair Janet Yellin as Fed alternate FOMC member in 2008, before she became Fed Chair.

Here is Professor Jeremy Siegel of the University of Pennsylvania’s Wharton School highlighting the Fed’s Folly: CLICK HERE

Watch “Mr. 100% Certain,” former Fed chair Ben Bernanke in July 2005: CLICK HERE

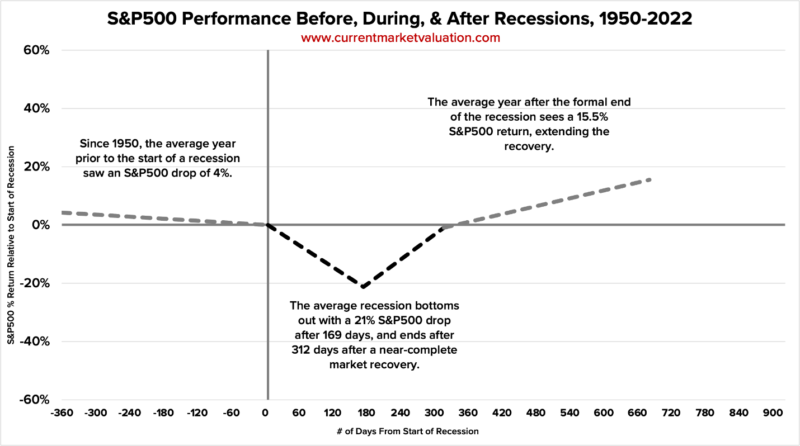

WHY WE ARE LONG TERM PERMABULLS:

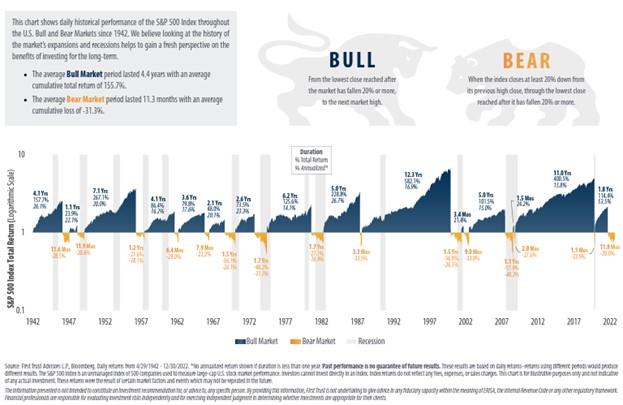

The chart below shows the history of the long-term equity market. In retrospect it is essentially one long bull market interrupted by periodic declines. Note the width of the blue and orange sections indicating the time duration of each cycle, and the height / depth of each which indicates the magnitude of the movement.

IMPORTANT PERSPECTIVE: There are not many problems in life that are resolved simply by patience and the passage of time. Most health problems, business issues or relationship challenges for example, get worse if unattended as time passes. Bear markets within a diversified portfolio of select equities is one of the very few that heals itself, provided the investor can withstand the temporary pain of declines in value. In fact, over the past 100 years, there was not been a single geopolitical or economic event that derailed the fundamental long term bull market or the stellar returns that it delivered to those who stayed the course.

THE HISTORY OF MARKET DECLINES AND SUBSEQUENT RECOVERIES:

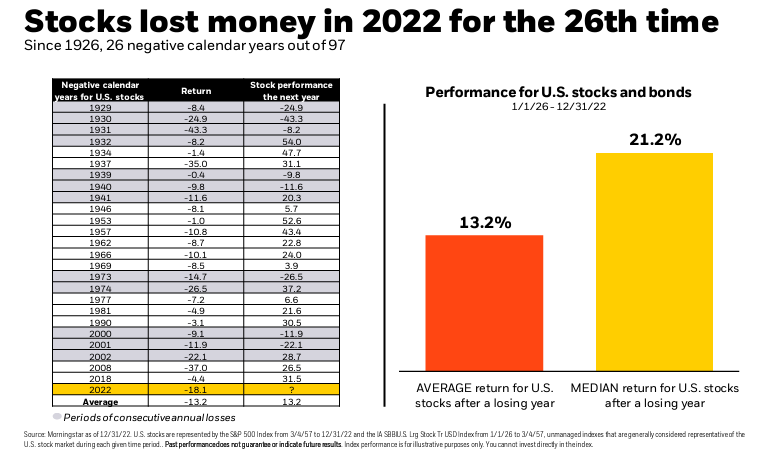

THE MARKET SEES INFLATION RETURNING TO BELOW 3% ON AVERAGE OVER THE NEXT 10 YEARS:

Amidst all the negative news and bearish projections, contrarian ideas have merit, if only to provide a sense of balance:

Here are 7 reasons to be optimistic about the economy and markets

-

Inflation is already declining in most critical areas

Home sales dropped 35.1 percent year-over-year in November, according to Redfin — the largest drop recorded by the brokerage since it began tracking sales in 2012.

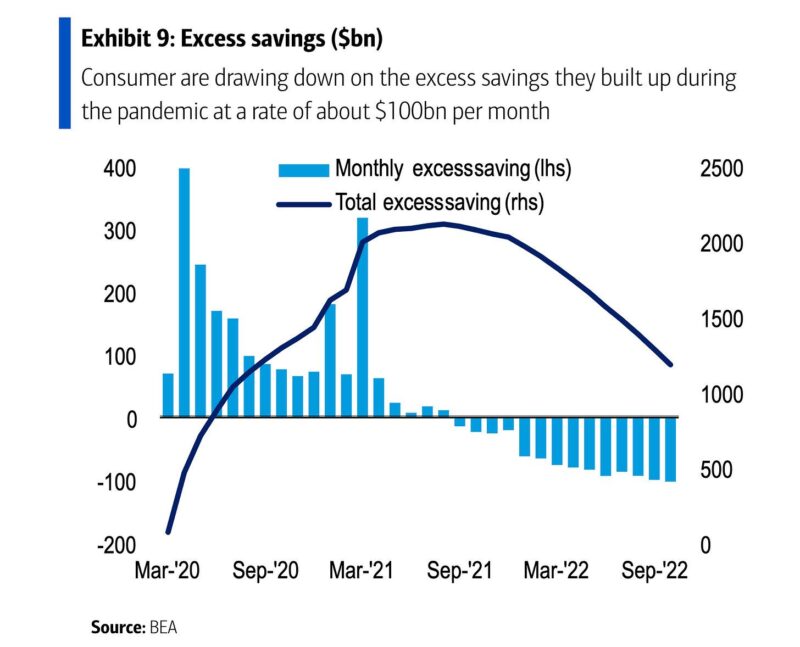

2. Consumer finances are very strong

Consumers are still sitting on about $1 trillion in estimated excess savings — the extra cash consumers have piled up since February 2020, thanks to a combination of government financial support and limited spending options during the pandemic. Keep in mind that the US economy is around 70% consumer-driven.

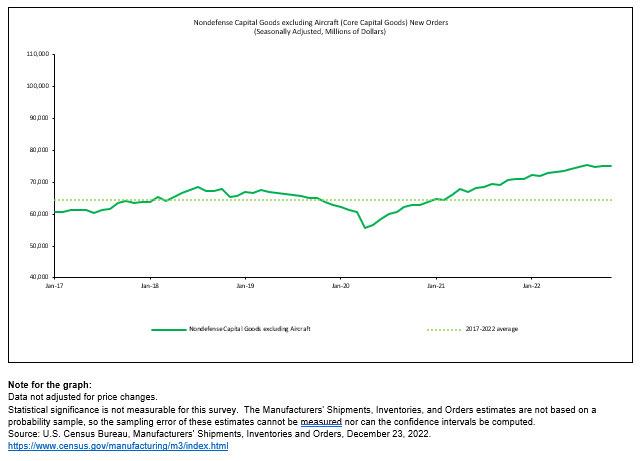

3. Businesses are investing at a near-record rate

Orders for nondefense capital goods excluding aircraft — i.e. core capex or business investment — climbed to a near-record $75.2 billion in November.

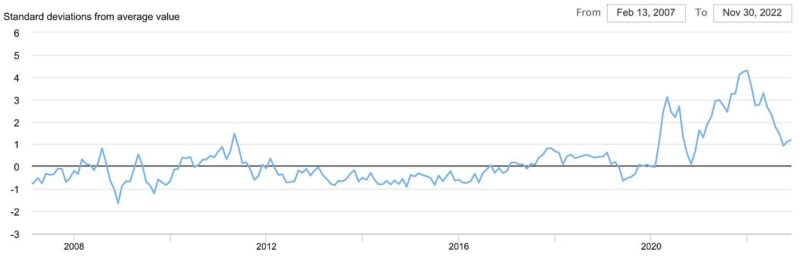

4. Supply chains have improved significantly

The New York Fed’s Global Supply Chain Pressure Index1 — a composite of various supply chain indicators — is now at levels last seen in late 2020 and is way down from its December 2021 supply chain crisis high.

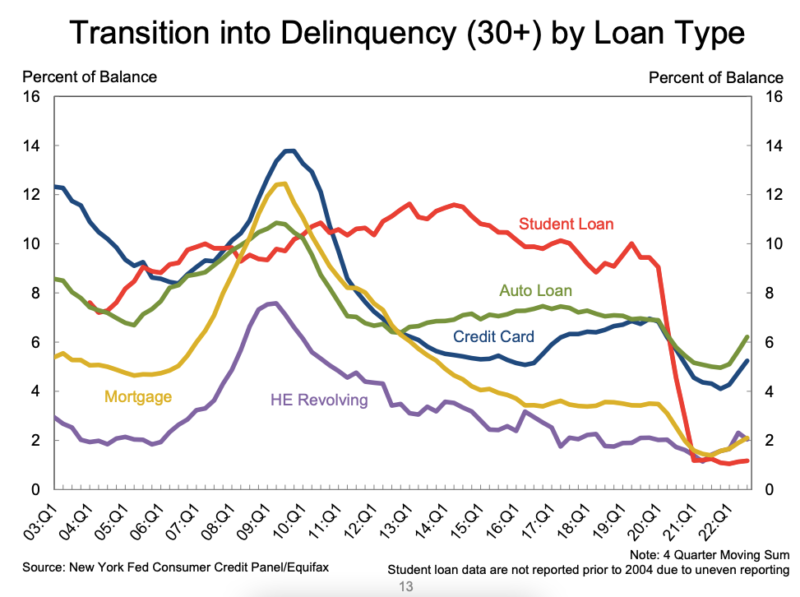

5. Household debt delinquencies are low

While debt delinquency rates are ticking up, they’re below pre-pandemic levels. In other words, delinquencies appear to be normalizing from very low levels.

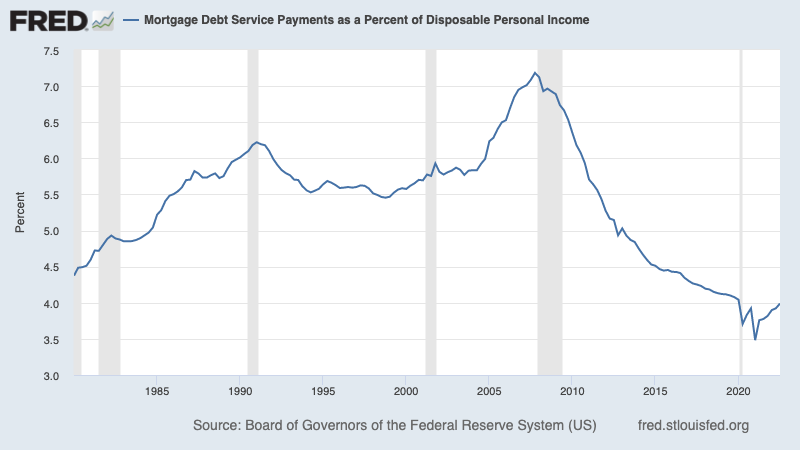

6. Mortgage payments are manageable

Mortgage rates surged in 2022 while home prices were near record highs. But this is not a repeat of the early 2000s housing bubble, when homeowners unable to make payments defaulted in droves. Current mortgages were largely supported by higher credit scores and at low fixed rates.

Today, mortgage debt service payments are historically low relative to disposable income, according to Federal Reserve data.

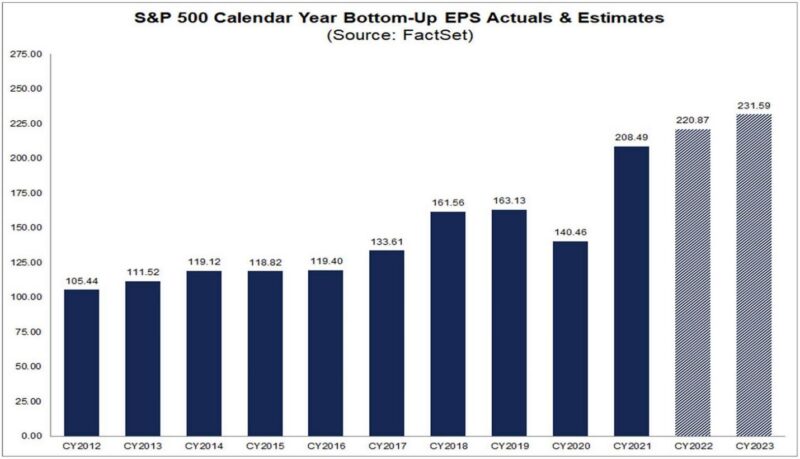

7. Corporate earnings are expected to be high although growing at a reduced rate – and if there is a decline it is not expected to be significant

Despite months of downward revisions to expected earnings, earnings are expected to be near record levels.

According to FactSet data as of December 15, analysts believe we’ll learn that S&P 500 earnings grew in 2022 and 2023 when it’s all said and done.

Thank you for entrusting your nest-egg to our stewardship. Please contact us if there is any change in your situation that impacts the allocation of your portfolio or any other aspect of your financial life that you wish to have us review with you. As trained Personal Financial Planners, our team stands ready to provide guidance and counsel in all related matters.

TAX LOSS HARVESTING: Over the past several months you may have noticed that we have been trading certain of your positions more frequently than we normally do. That has been primarily because of us locking in a potentially tax-beneficial loss – and replacing the investment with an alternative that is economically similar. That allows us to “tax loss harvest” – a classic way to turn lemons into lemonade.

INVESTING IN ALTERNATIVES: Over the past year we have been selectively introducing investments in income producing real estate funds and private credit funds to enhance cash flow and diversify into uncorrelated or low-correlated investments. These have done remarkably well, and we plan to expand our exposure to these categories. If you wish to include this category in your portfolio, please contact us immediately.

Sincerely,

Your RVW Wealth Team:

Selwyn Gerber, Jonathan Gerber, Stephen Seo, Loren Gesas, Mary Ann Moe, Simon Liu, Lisa Blackledge, Jesse Picunko, Ofer Ben-Menahem, Dylan Scott, Teresa Green, Shelly Moore, Simmons Allen, Morgan Vickers, Kelly Sueoka, Shuey Wyne, Erik Stevens, Jeff Farrell, Drew Wallis, Denise Magilnick, Hamed Sepehri, and Kelly Richardson.

FOR IMPORTANT CURRENT COMPLIANCE AND DISCLOSURE INFORMATION GO TO https://rvwwealth.com/compliance

NOTE: The information provided above is not complete, may be erroneous, and omits important data. The charts are estimates and may contain inaccuracies or distortions.

Read and rely exclusively on actual offering documents and on statements received directly from your custodian. Investments are not guaranteed and may lose value. Past performance is not indicative of likely future returns.